The majority of empirical research in accounting is frequentist in nature. The distinction between the Bayesian perspective and the frequentist perspective has been discussed by Berger (1985) at greater length. One advantage of Bayesian analysis is that by incorporating important prior information, it improves statistical inferences (Berger, 1985). In this spirit, Dechow et al. (2012) show that exploiting the inherent property of accrual accounting can improve the power and specification of tests for earnings management.

Bayesian hierarchical estimation is a way to account for cross-firm heterogeneity, which is not addressed in most structural estimations in accounting (e.g., Bertomeu et al., 2018; Zakolyukina, 2018; Du, 2019). Our estimation method, MCMC, is standard in many academic disciplines, but has been applied only recently in accounting research: Bernhardt et al. (2016) estimate the stickiness of analyst recommendations in a cross-section of analysts, while Zhou (2017) estimates the impact of investor learning on cross-sectional variations in the manager’s voluntary disclosure. Our study is the first to use the Bayesian hierarchical method to estimate firm- and time-varying earnings quality.

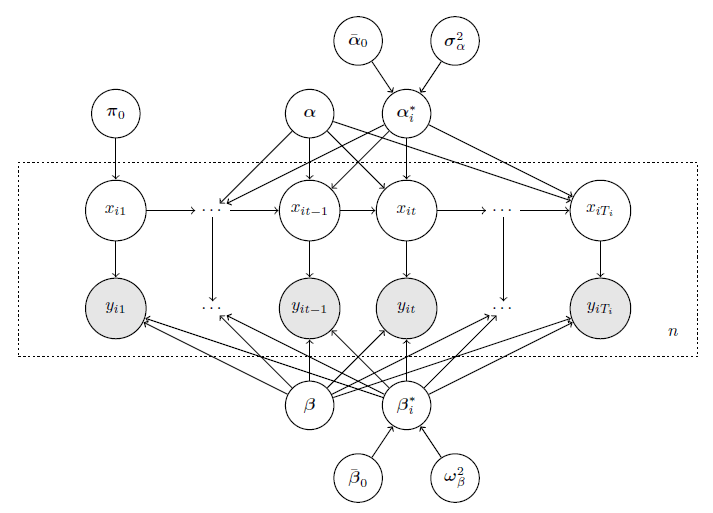

The Bayesian hierarchical framework of our study is illustrated below.

References:

Bernhardt, D., Wan, C., Xiao, Z., 2016. The reluctant analyst. Journal of Accounting Research 54, 987–1040.

Bertomeu, J., Ma, P., Marinovic, I., 2018. How often do managers withhold information? Working paper, University of California at San Diego.

Dechow, P., Hutton, A., Kim, J., Sloan, R., 2012. Detecting earnings management: a new approach. Journal of Accounting Research 50, 275–334.

Du, K., 2019. Investor expectations, earnings management, and asset prices. Journal of Economic Dynamics and Control 105, 134–157.

Zakolyukina, A., 2018. How common are intentional GAAP violations? Estimates from a dynamic model. Journal of Accounting Research 56, 5–44.

Zhou, F., 2017. Disclosure dynamics and investor learning. Working paper, University of Pennsylvania.